Economic growth continued in early 2008, even as pressure in the housing market intensified. That summer, oil reached $147 per barrel, equivalent to about $222 today, while gasoline rose above $4 per gallon, equivalent to about $6 today. The surge quickly strained household budgets and business operations. It also limited the Federal Reserve’s willingness to lower interest rates and provide support to a weakening economy. After several relatively stable years, investors suddenly found themselves confronting a sharply different economic backdrop. Could oil become a tipping point in 2026 as well?

Oil remains one of the world’s foundational commodities. It touches transportation, manufacturing, shipping, and nearly every part of supply chains. Even if U.S. production remains stable, domestic prices can still rise when global buyers bid more aggressively, tightening conditions at home. We saw that in 2022. At the time, elevated household savings helped support resilient consumer spending in the United States. Those excess savings have now largely been exhausted.

Higher oil prices act much like a tax on the economy. They work their way through fuel costs into the price of food, construction materials, airfare, and countless other goods and services. As households spend more on necessities, they are often forced to spend less on discretionary items.

That dynamic also complicates the Federal Reserve’s job. A rise in energy prices can keep inflation elevated even as growth begins to slow, making it questionable for policymakers to respond with lower rates. That is one reason major energy shocks have preceded several recessions. Central banks cannot easily support the economy when doing so risks intensifying inflation.

While investors often debate what the Fed should do, what matters most is what policymakers actually do and how markets respond. The Fed controls short-term interest rates, but longer-term rates often matter more, and those are set by investors in the bond market.

A more likely sequence is this: Higher energy prices push inflation higher, which puts upward pressure on interest rates. Higher rates reduce borrowing and spending, which slows income growth and weakens demand. Over time, that softer demand helps ease price pressures. But the adjustment does not happen immediately.

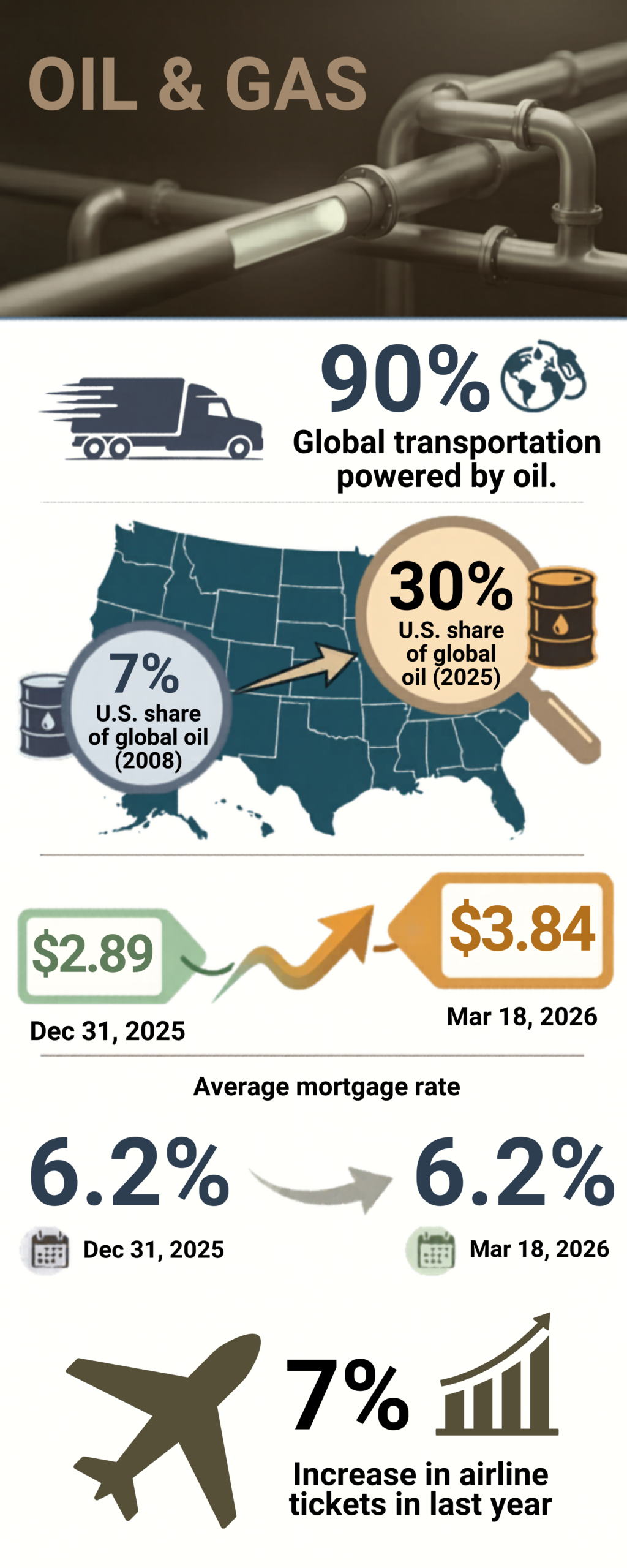

There are also meaningful reasons to believe 2026 may differ from past oil shock episodes. In 2008, U.S. oil supply represented only 7% of global demand. Today, it accounts for roughly 30%. That gives the United States a stronger position and suggests the country may benefit more from higher prices than it did in the past. Just as important, the increase in oil prices so far is not nearly as severe as the run-up that occurred in 2008.

In this environment, we will continue to monitor oil prices and interest rates closely. Our focus remains on maintaining discipline, adapting to changing conditions, and preparing for the opportunities that periods of uncertainty can create.