Recently, my children asked if I would buy them orange sorbet. At that moment, orange sorbet sounded pretty good to me, too, so I agreed. I jumped into my car and headed to the store. Somewhere along the way, I answered a phone call. Buying ice cream has become second nature to me, so without thinking, I made my purchase and walked back to my car, fully focused on my phone conversation.

As I slid into the driver’s seat, sorbet in hand, I first noticed the air freshener dangling from the rearview mirror. I don’t like rearview mirror ornaments. Then I saw the woman’s sweater on the passenger seat, followed by the pink polka dot steering wheel cover. You might be surprised by how long it took me to process this shocking, unexpected information. This was not my car, but someone else’s that happened to look very similar from the outside.

The moral of my story: details matter. A vehicle may look right from the outside and still be wrong. Financial strategies work the same way. What appears smart at first glance can become a costly mistake when the surrounding details are ignored.

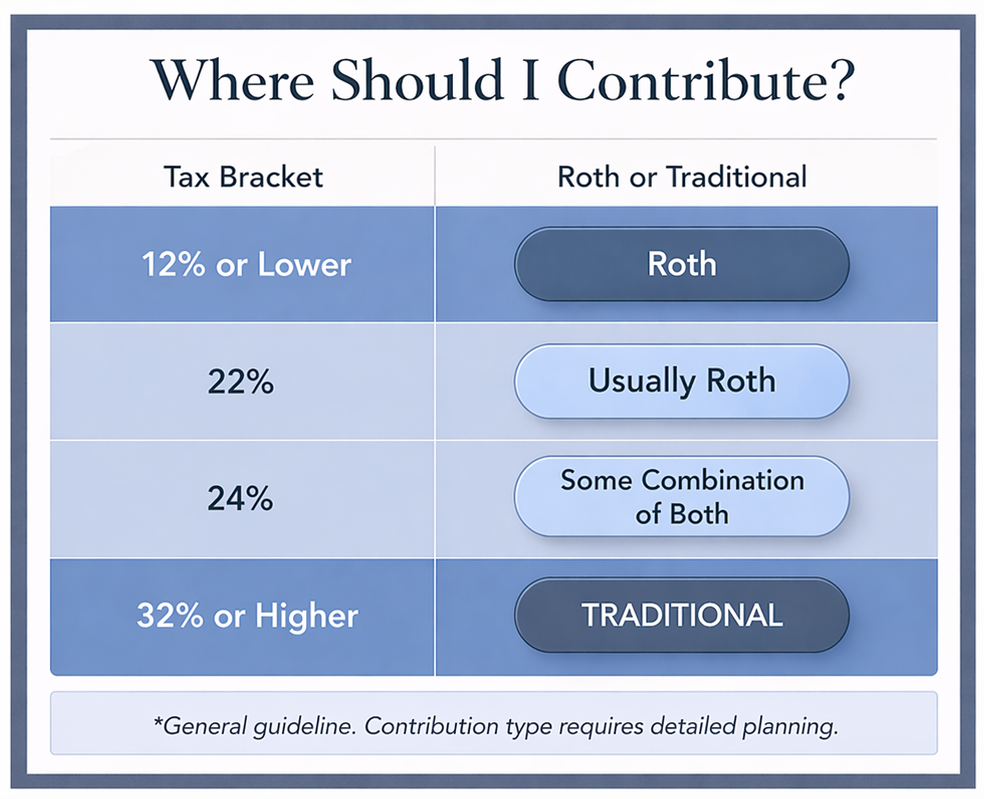

That is especially true when it comes to Roth conversion decisions. A Roth conversion allows an investor to move assets from a tax-deferred account into a Roth. In exchange for paying tax on the converted amount, they gain the benefits of tax-free growth, reduced required minimum distributions, and tax-free transfers to beneficiaries. It is easy to see why Roth conversions generate so much enthusiasm.

However, a Roth conversion will only create a benefit if executed in the right situation, in the right amount, and in the right year. That requires careful awareness of current and future tax brackets, Social Security, and Medicare.

Roth conversions are beneficial for many investors, but not all. Tax-free growth sounds like a clear win, but the math often proves otherwise. The excitement around Roth accounts has convinced many to move money into them regardless of their tax bracket, or to convert traditional assets the moment they find themselves in a lower bracket. In other words, many investors see what appears to be the right financial vehicle but fail to fully evaluate the details.

A Roth conversion can become more expensive when it is done in the wrong year. A year that includes high income can make a conversion far less attractive than it first appears.

I once had a client in the 37% tax bracket. They came to me interested in doing Roth conversions. Because there was a high expectation that they would be in a lower tax bracket in retirement, I strongly recommended against it. This client was so focused on the benefits of the Roth that they failed to notice the pink polka dot steering wheel cover. The conversion was the wrong financial vehicle for them.

A Roth conversion can sometimes create more taxes than expected because the converted income does not simply fill up a tax bracket. It can ripple through the rest of the return by causing more Social Security to become taxable, triggering higher Medicare premiums, and increasing the true cost of the conversion.

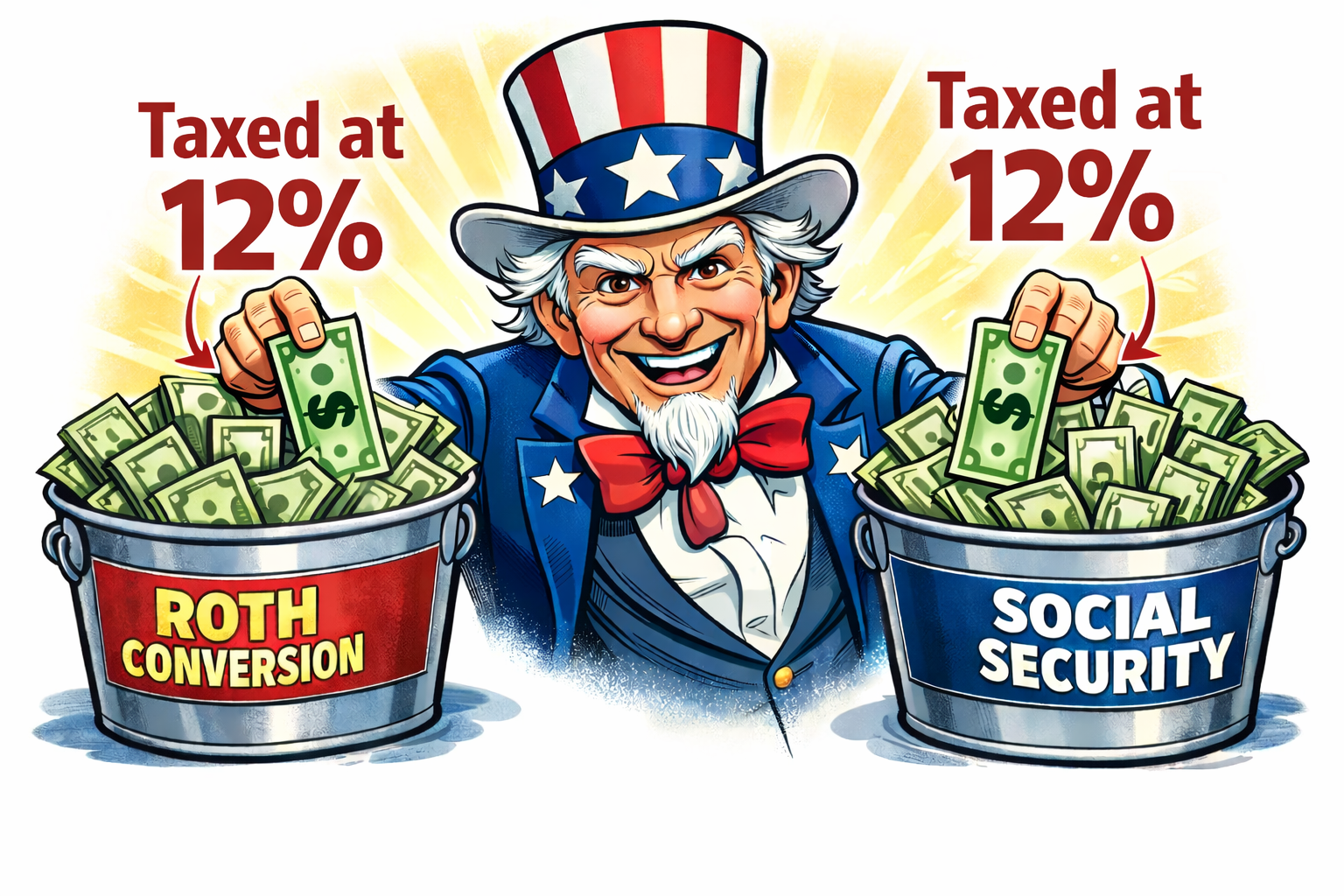

For investors in a low tax bracket who are receiving Social Security, a Roth conversion can create a costly surprise. In some cases, each dollar converted can cause up to one additional dollar of previously untaxed Social Security benefits to become taxable, until the maximum taxable amount is reached. This effectively increases the tax impact of the conversion. You may be in the 12% bracket, but a $10,000 conversion could increase your federal tax liability by closer to $2,400. That makes the 12% bracket feel more like a 24% tax on the converted amount.

Medicare must also be considered. Suppose someone is on Medicare and executes a large Roth conversion. Even if that conversion was a smart long-term move, it may raise their income enough to push them over an IRMAA threshold. They now pay more each month for Medicare Part B and Part D. In 2026, the standard Part B premium is $202.90 per month, but higher-income beneficiaries can pay up to $689.90.

If it is the backdoor Roth conversion strategy you’re considering, you’re playing with after-tax dollars. Social Security and Medicare won’t factor into the equation, but now you must account for any existing pre-tax IRA balances due to the pro rata rule. When those balances exist, this strategy can backfire by making a portion of your conversion taxable at your current, often higher, tax rate.

If you are considering a Roth conversion, don’t jump in blindly like a distracted parent rushing to satisfy a sugar addiction. Speak with us. We can help analyze the details, explain the tax consequences, and determine whether a Roth conversion is the right vehicle for you.