In order to stimulate the economy after the Great Recession of 2008, the Federal Reserve kept interest rates historically low for much of the period that followed. This prolonged environment of low rates affected nearly every area of financial markets. Mortgage rates were low, but so were returns on investments that paid interest. Traditionally safer assets such as bonds, certificates of deposit (CDs), and money market accounts often produced negative returns after taxes and inflation. In recent years, however, higher interest rates have significantly changed the role of these assets.

Higher interest rates have created greater opportunities for conservative investors to grow their portfolios with less risk. CDs have offered attractive returns recently, with yields ranging from 3% to 5%, compared with 1% or less during much of the post-2008 period. Money market accounts have also become a more compelling option.

The greatest impact of higher rates for investors is that they can once again feel comfortable holding larger cash reserves. During the low-interest-rate environment following 2008, many investors felt compelled to invest more aggressively in order to keep pace with inflation, even while their tolerance for risk was low.

Another significant retirement planning factor has been the changing bond market. After 2008, bond yields experienced a historic decline, reaching record lows in August 2020. In recent years, bond yields have risen sharply as central banks increased interest rates to fight inflation. These higher yields have allowed retirees to use different bond strategies to generate income while leaving more of their principal intact.

Early in retirement, investors need their portfolios to continue growing while also producing distributions to support spending needs. Higher-yielding bonds can help provide that income when the portfolio is balanced against inflation, taxes, and long-term growth needs.

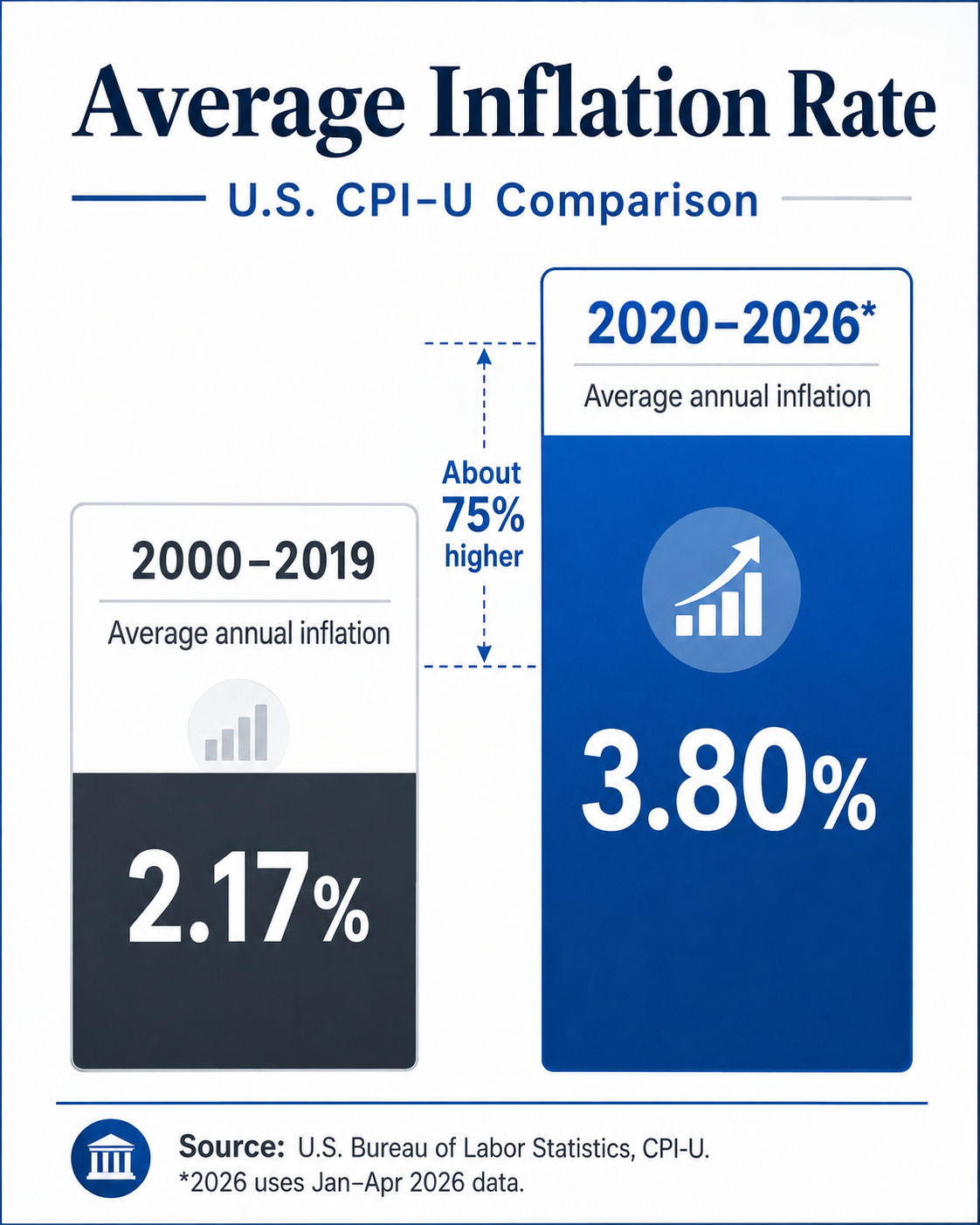

But higher interest rates have come for a reason: to fight higher inflation. For years, retirement advice focused heavily on maximizing returns and accumulating assets. Now, there is a greater need to focus on inflation resilience and tax management. While a conservative investor may be pleased to earn 3% on a high-yield savings account, if inflation is 4%, purchasing power is still in decline. These higher-yielding accounts have a new challenge: how to preserve real value while still supporting income needs.

The good news is that with careful planning and disciplined tax management, retirees can position themselves to meet these challenges successfully. Strategically placed assets can help fight these new battles while still taking advantage of higher rates. Financial advisors are increasingly adapting retirement income strategies to reflect this changing environment. With the right plan, higher interest rates can become more than a challenge. They can become an opportunity.