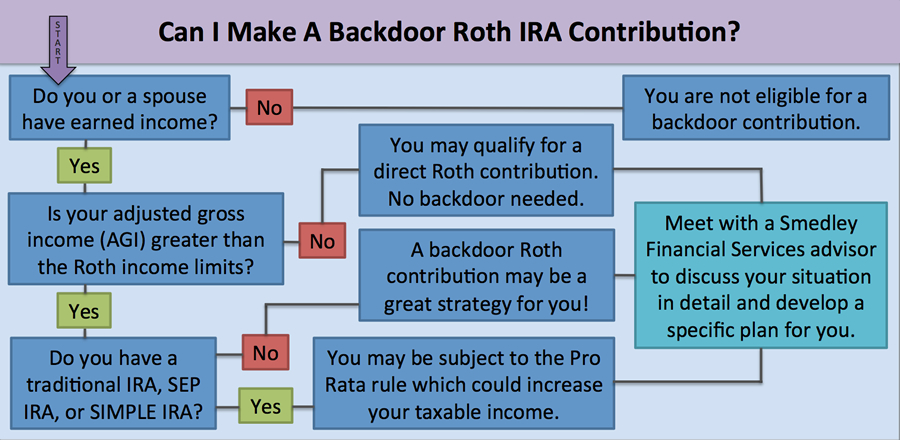

The Roth IRA is my favorite retirement savings account. It offers compelling benefits, including tax-free growth, no required minimum distributions (RMDs), and better terms for heirs. Unfortunately, if your income exceeds the Roth IRA limits, you are not eligible to contribute.

There is a strategy for high-income earners that avoids the Roth income limits entirely. This strategy is known as a backdoor Roth contribution.

A high-income earner can always make a non-deductible contribution to their traditional IRA, up to the contribution limits. They are also allowed to convert traditional IRA assets to Roth IRA assets. The backdoor Roth takes advantage of these rules. The strategy requires making a non-deductible contribution into a traditional IRA and then immediately converting those assets to Roth. It is a valuable move under the right conditions.

But the backdoor Roth contribution is not entirely unguarded. If you have tax-deferred assets in a traditional IRA, SEP IRA, or a SIMPLE IRA, the backdoor contribution may result in undesired taxation. This is because the Pro Rata Rule will calculate taxes due from a backdoor contribution based on all IRA assets proportionally. If you have tax-deferred IRA assets, I recommend caution with a backdoor Roth contribution.

The types of accounts used to save for retirement can greatly impact a financial plan. Are you using the best accounts for your situation? Is there a strategy you are unaware of that may be advantageous? Have you had a change in income or employment? We recommend you review your retirement plan with your advisor regularly to ensure you are taking advantage of the best options available to you. Call us today!