With interest rates at historic lows, there is a lot of talk about refinancing current mortgages. If you own a home, this is a great time to evaluate your loan and ensure you have the best terms available.

While interest rates across all loan types may be low, not all loans are the same. Here are some tips to help you understand the nuances and determine if you should refinance a first mortgage, take a home equity loan, or open a home equity line of credit.

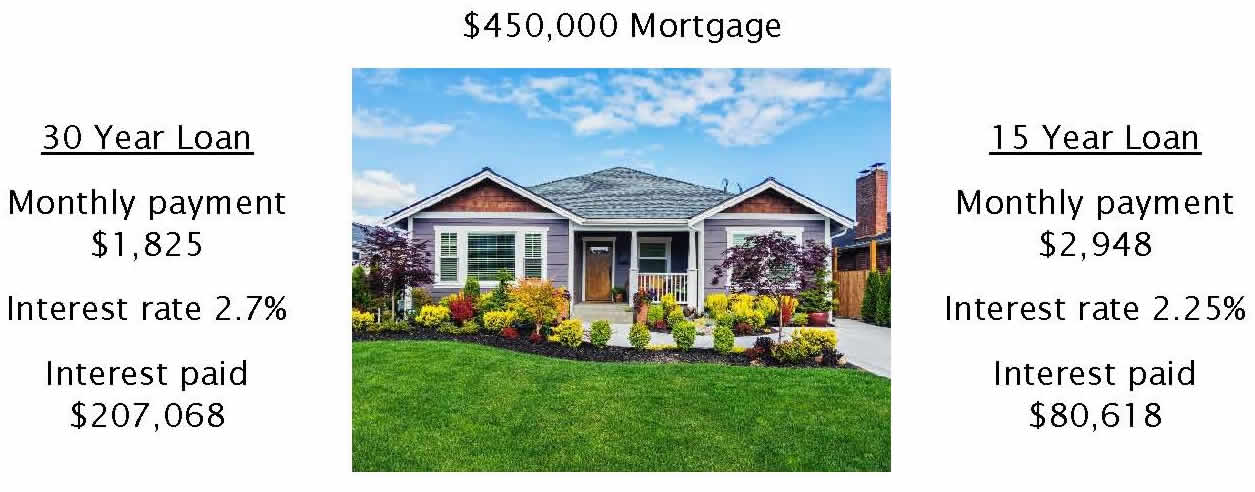

Mortgage loans, referred to as first or second mortgages, are paid over a fixed period of years: 30, 20, 15, 10, or less. The interest rate can be fixed for the entire loan term or variable, changing based on the Prime rate. While rates are low and you can spread the payments over many years, keep in mind that you will pay less in overall interest if the loan term is shorter, say 15 years, versus a longer-term, say 30 years. While the payment may be higher, the difference can save you tens of thousands of dollars.

In this example, the savings for taking the shorter-term loan is $126,450. Not to mention that you are out of debt in half the time. This example does not include taxes, insurance, or any associated closing costs.

I realize that locking yourself into a higher monthly payment may limit your monthly discretionary cash flow. It does not have to be all or nothing. Choose the mortgage term that helps you save as much as possible and still maintain a flexible cash flow—making an extra principal payment when possible will save you interest and shorten the term of the loan.

Home equity loans allow you to borrow based on the equity in your home. These loans are gaining in popularity as home values continue to skyrocket. The increasing value of your home has likely created a pool of equity. Tapping into that equity for home improvements, such as upgrading a kitchen or adding a room or garage, is a favorable option compared to borrowing on a signature loan or credit card. Home equity loans have a fixed loan period, up to 10 or 15 years, and offer both fixed and variable interest rates.

Home Equity Line of Credit loans, referred to a HELOCs, allow you to use the equity in your home in another way. These loans offer a fixed credit limit that you can tap into as needed. The interest rate is variable and can increase or decrease over time. Repayment of the loan is more like a credit card in that there will be a minimum required payment each month, such as 1.25% of the loan balance. The trick here is discipline. You must form a plan to get the loan paid in a certain period. Otherwise, you will find that making the minimum payment has cost you a great deal of money.

After looking at the loan options available, consider what you will pay in closing costs. You may be required to pay for an appraisal, and sometimes a lower advertised rate requires that you pay points to secure the loan. This means you will have to come up with a percentage of the loan amount at closing.

Choosing between a fixed or variable rate can be difficult. I will say this; it is more likely that interest rates will go up in the future rather than down. Variable rates are generally lower than fixed rates and may make sense if it is likely that interest rates will go down. In the current environment, fixed rates are so low that you can feel confident you are locking in a good rate for the term of your loan.

Before you move forward, take the time to compare the facts on your current loan versus a new loan. The closing costs associated with a new loan may cost you more than keeping the current one. If you have questions, please reach out to our team. We can help you assess your options and determine the best course of action.