This week has been nothing short of stunning, marked by significant market volatility and a sense of delusion among some investors. Optimism reigned as companies like Tesla, despite lackluster Q4 results, moved up. Speaking of Tesla, Alexander Potter, an analyst at Piper Sandler, noted, “Q4 results weren’t great, but who cares? Elon has never sounded so bullish.” This sentiment was echoed after Meta reported that it was no longer buying back shares of its company and the CEO, Mark Zuckerberg, was selling. Apple reported declining iPhone sales, which have not grown in three years. Investors initially pushed the stock price up by 5%, only to see all those gains evaporate within 24 hours. Retail investors are seeing the glass half full, but reality hit back hard this week.

Americans are spending more than they save, with rising prices boosting company profits. Tariffs are back, and despite skepticism, President Trump confirmed a 25% increase, causing market volatility. Stocks dipped after a brief rebound, but it was a positive week for my recommended overweights.

Gold hit all-time highs, but no changes were made. Oil and energy stocks are down, but recommendations remain unchanged. Bonds bounced back, and I’m watching for opportunities in bonds, small-cap stocks, and internationals. I’ll add significantly when the time is right.

The key macroeconomic question for 2025 is, “What will the new administration do about government debt?” We’ll get our first clue on February 5th. Government spending has been propping up the economy, so any changes will have a big impact.

Scott Bessent, the new Treasury Secretary, has criticized his predecessor for issuing a lot of short-term debt, suggesting it was politically motivated. This week, Bessent will outline his plans.

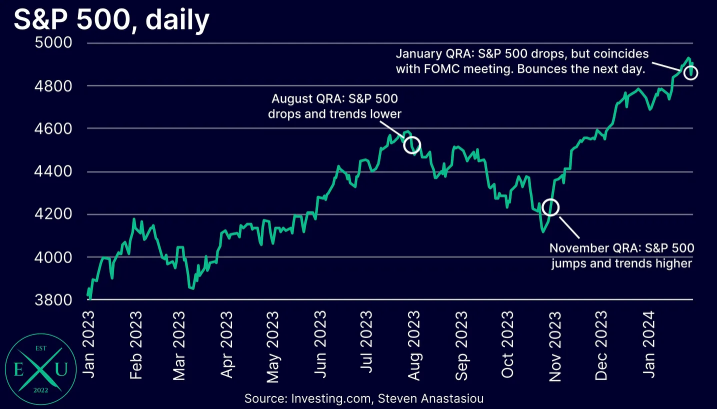

The U.S. Treasury will announce its Quarterly Refunding Announcement (QRA) on February 5th. The Treasury wants its checking account (TGA) at $850 billion. The big question is how much intermediate and long-term debt will be issued, which affects market liquidity. This triggered a 10% market selloff in August 2023 and a subsequent rally three months later.

I’m staying invested according to my benchmarks, with overweight in energy, healthcare, and gold. Bonds are showing positive momentum despite inflation issues, and the U.S. dollar seems to be topping out. This is a big opportunity, but I will wait for the QRA before buying more.

What the government says it will do next may be more important than what they have already announced. Stay tuned.

President Trump is back, shaking up the markets with tariffs. Investors doubted him, but he followed through, causing a minor crash. Tariffs on Mexico and Canada were suspended for 30 days, and markets bounced back. Following market moods too closely led some investors astray.

Tariffs bring concerns of inflation and recession. Fidelity Investments notes that while some prices rise, tariffs are generally deflationary. About one-third of the cost hits consumers, one-third hits companies, and one-third the currency, potentially reducing GDP by half a percent.

Oil prices doubled in the early 2000s without crushing the economy due to gradual increases. The real issue is whether wage growth keeps up with inflation. Small business earnings are solid, and if growth continues, higher wages could stabilize the economy and stocks.

While waiting for these opportunities, I stayed invested in large-cap stocks in the U.S. The largest stocks have been the place to be, dominating the market in a way rarely seen since 1998 and 1999. When the tide turned in 2000, there were numerous ways to add value as an active manager. I know because I started my career in January 2000.

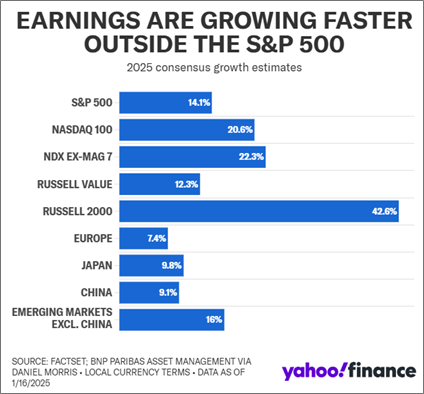

Small company stocks are under scrutiny. It has been years since they outperformed large company stocks. They are still hurting from higher interest rates and desperately need to turn a profit. Analysts believe 2025 will be the year they turn it around, potentially resembling the year 2000. However, I remain unconvinced and will continue to monitor this closely. What about bonds? If bond momentum remains positive on Wednesday, then I am interested.