Negativity and false information about renting are unjustified, especially now. Homeownership offers benefits, but first-time home buyers may do themselves a favor–both emotionally and financially–if they ditch the idea that renting is always bad.

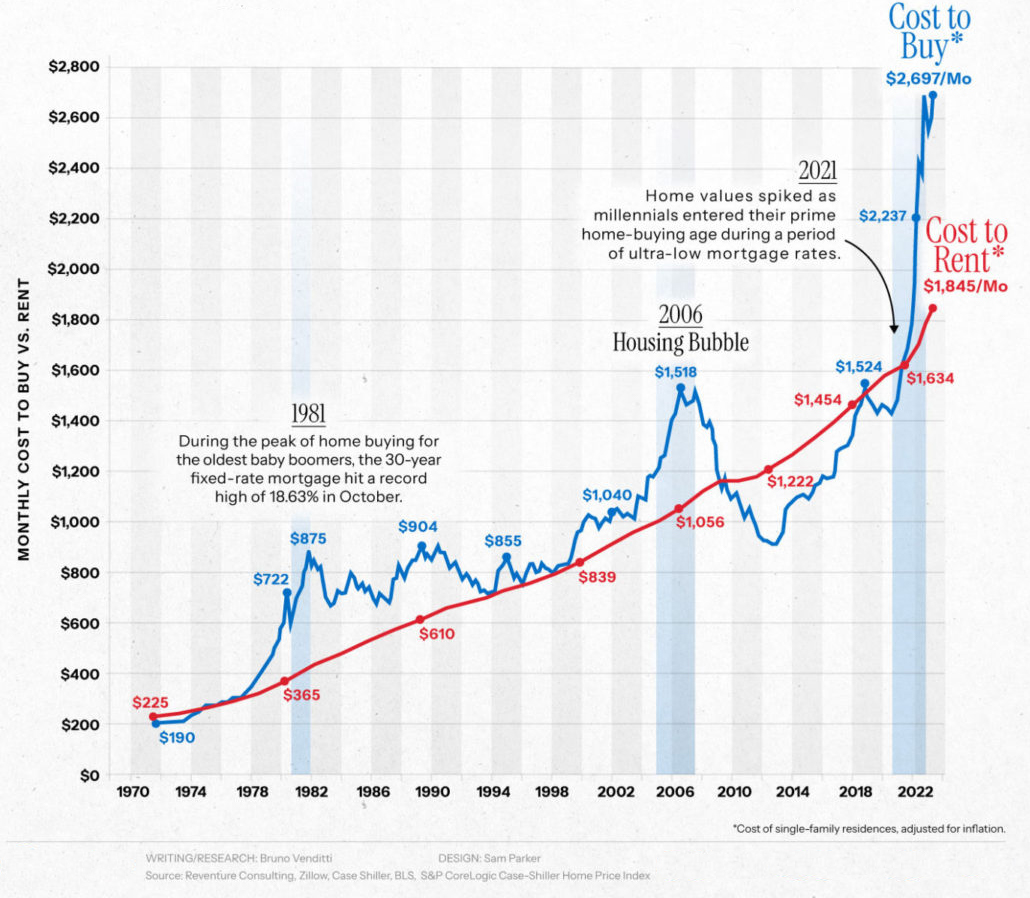

Sticker prices on starter homes have been surging. The pain doesn’t stop there. Hidden costs of homeownership are skyrocketing.

According to a study by Bankrate, U.S. homeowners are paying an average of $18,118 per year on property taxes, homeowners’ insurance, maintenance, energy, and other home expenses. This is a 26% increase from four years ago when it cost $14,428 annually to maintain a home.

Those who stretch their finances to get into a home now may later find the hidden expenses crushing their budget. Even for those who can afford the higher costs, the lifestyle sacrifice required to meet them may be significant.

The alternative to buying a home is renting. But isn’t that just paying someone else’s mortgage? How can this be a good alternative if, in the end, the renters have nothing to show for it?

Renting is not throwing away money, financially unwise, or something to be ashamed of. Many say they are worried that they, their children, or their grandchildren will never be able to afford a home. But, if buying a home leads to a financially worse situation, why is homeownership the better path?

I’m not suggesting anyone sell their home only to rent. I’m not saying that homeownership isn’t ideal. I am saying that for those looking for a place to live, renting may be the better financial choice–even if they can afford the price of a home. The stigma around renting is oversimplified, inaccurate, and potentially harmful.

Owning a home can be a significant blessing. Buying a home under the wrong financial conditions can be a curse. One should only buy when it makes sense financially.

Renting provides greater flexibility for future locations. It does not require a large down payment, has lower liability, and avoids unexpected maintenance. There are no property taxes, lower insurance costs, and possibly even lower utility bills. This all equates to lower expenses and higher monthly investment capital.

Suppose individuals today take the money they save by renting and invest it in the stock market. In that case, the data shows that they will be better off 30 years from now than if they purchased a home instead – assuming no significant changes in the current variables. And if economic variables do change, the renter has the flexibility to buy at that point and with greater liquid savings.

Let’s not pressure those who can’t afford a home by perpetuating false information about renting. Let’s focus on the upsides and financial opportunities that renting currently offers, and celebrate that a blown-out water heater is fixed by just a quick phone call to the landlord.