Many Americans plan to fund retirement by tapping the equity in their homes. Now, politicians are floating the reverse: using retirement savings to buy homes. It is the latest attempt to resuscitate a housing market that has stalled under the weight of its own excesses.

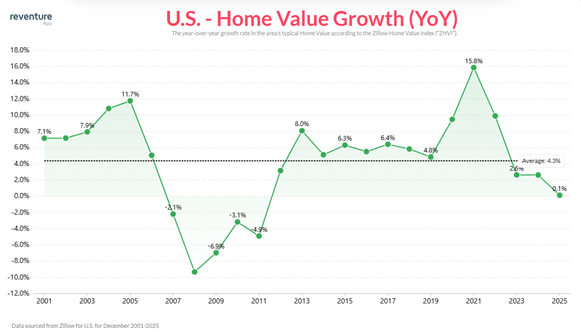

Pending home sales fell 9.3% nationally in December, with declines across every region of the country.1 Sellers outnumber buyers by 600,000, allowing discounts to original listing prices on 62% of purchases last year.2 For the U.S. economy, housing is a core engine of growth. When it slows, policymakers start suggesting solutions.

Penalty-free 401(k) withdrawals for home purchases would boost demand and put a short-term floor under prices. They would also drain retirement savings, trigger taxes, and destroy decades of compounded market returns.

Many savers can already borrow from a 401(k) and avoid penalties, but it still reduces growth and tightens monthly cash flow. Unless the deal is extraordinary, this is trading long-term security for short-term relief.

A 50-year mortgage sounds clever, as longer terms mean lower monthly payments. Auto loans have crept from 5 to 7 to 10 years. But a 50-year loan dramatically increases risk for lenders. Wall Street doesn’t want it, and neither do lenders. Even the U.S. Treasury won’t issue bonds longer than 30 years.

Lower mortgage rates are a win for current and aspiring homeowners. These rates are comprised of long-term interest rates, a housing market spread, and borrower-specific risk. Treasury yields dominate, and they move with global financial flows, not wishful thinking.

The government can try to compress the spread by stepping into the mortgage-backed securities market through Fannie Mae and Freddie Mac. Even talking about MBS purchases has nudged rates down a little.

Another proposal is to stop large investors from buying single-family homes. Fewer well-capitalized bidders might ease pressure on prices. Would it have unintended consequences?

While young, aspiring homeowners have been waiting for years for more affordable housing, nearly two-thirds of adults already own their homes and benefit from rising prices.3 Propping up those prices indefinitely becomes harder and riskier the higher they go.

Keep an eye on long-term rates in 2026. We hope to see them come down a little, especially if we can get them with continued economic growth and low inflation. Lower rates help buyers without punishing sellers.

For a deep dive into the housing market, listen to the Power Up Wealth podcast.