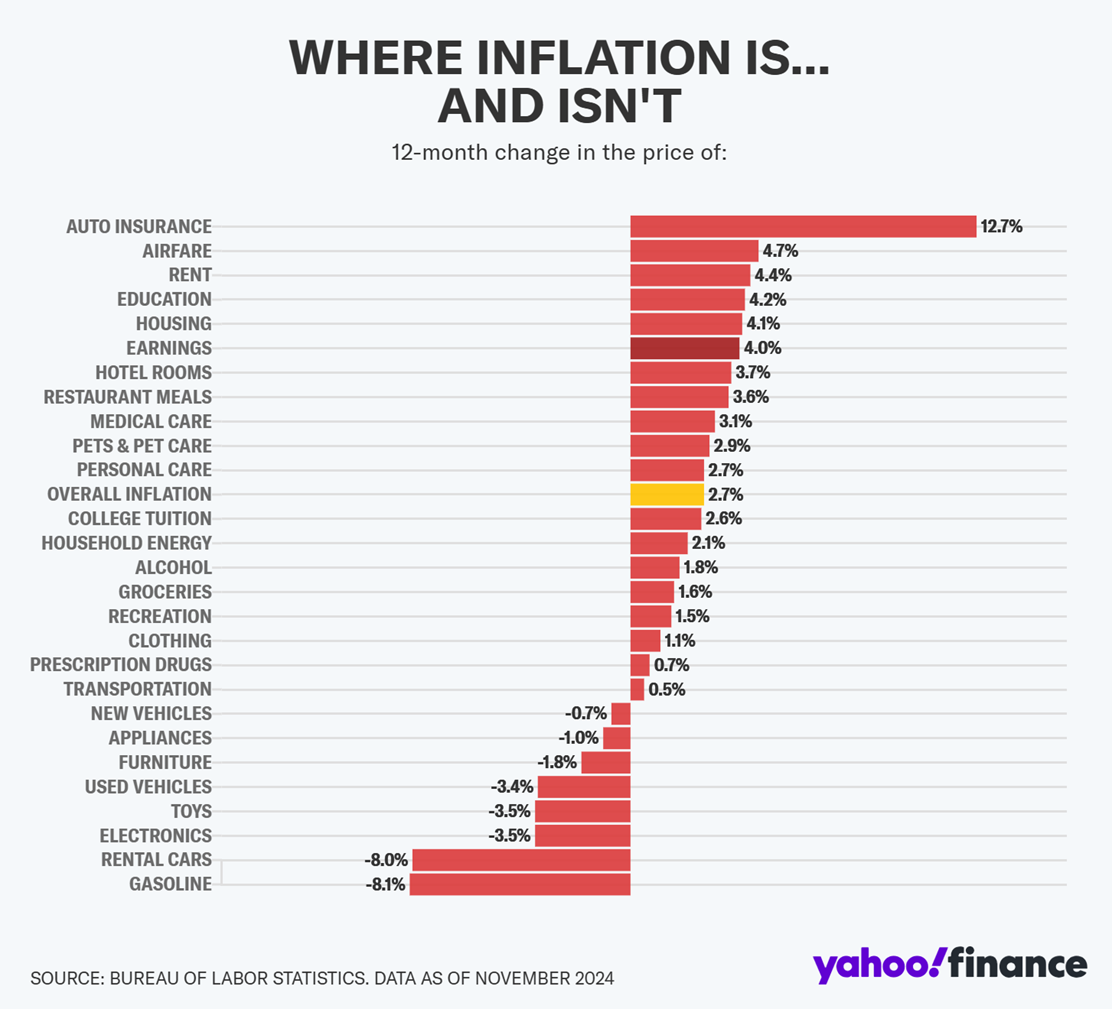

Inflation remains stubbornly high, around 3%, driven by rising food prices (notably eggs) and sustained by business services (insurance). The Federal Reserve’s 2% inflation target is out of reach and has been for nearly five years.

On December 18th, the market expects the Fed will lower the overnight rate by another 0.25%, totaling 1.0% in cuts over the past four months. Long-term rates have risen significantly as the Fed has lowered because bondholders are questioning the Fed’s commitment to its 2% target.

A more nuanced approach is better. The balance sheet, initially used to create inflation, hasn’t been adequately adjusted to control it. The Fed should cut rates and actively lower its balance sheet. That’s my opinion. It is not happening. It is also unlikely to happen. These are the three likely scenarios for this week:

- Rate Cut with Possible January Cut: The Fed lowers rates and indicates another cut in January if inflation isn’t a concern.

- Rate Cut with Data-Dependent Future Cuts: Fed lowers rates and signals potential cuts in 2025, pending further data.

- Rate Pause: Fed pauses rate cuts and monitors data into 2025.

A single rate cut won’t alter the economic trajectory but could influence markets temporarily. Stocks are more attractive in scenario one, while bonds are preferable in scenario three. Scenario two is the most likely outcome.

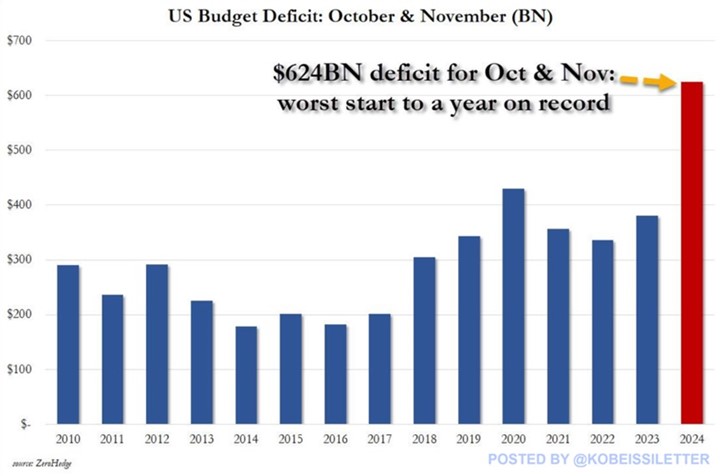

The economy is buoyed by substantial federal deficit spending, with the fiscal year starting in October. Many stock buyers are insensitive to stock prices, especially in December. Large publicly traded companies and 401(k) contributors are adding regularly regardless of what is happening. This works over the long term. The large flows may also be masking a growing weakness.

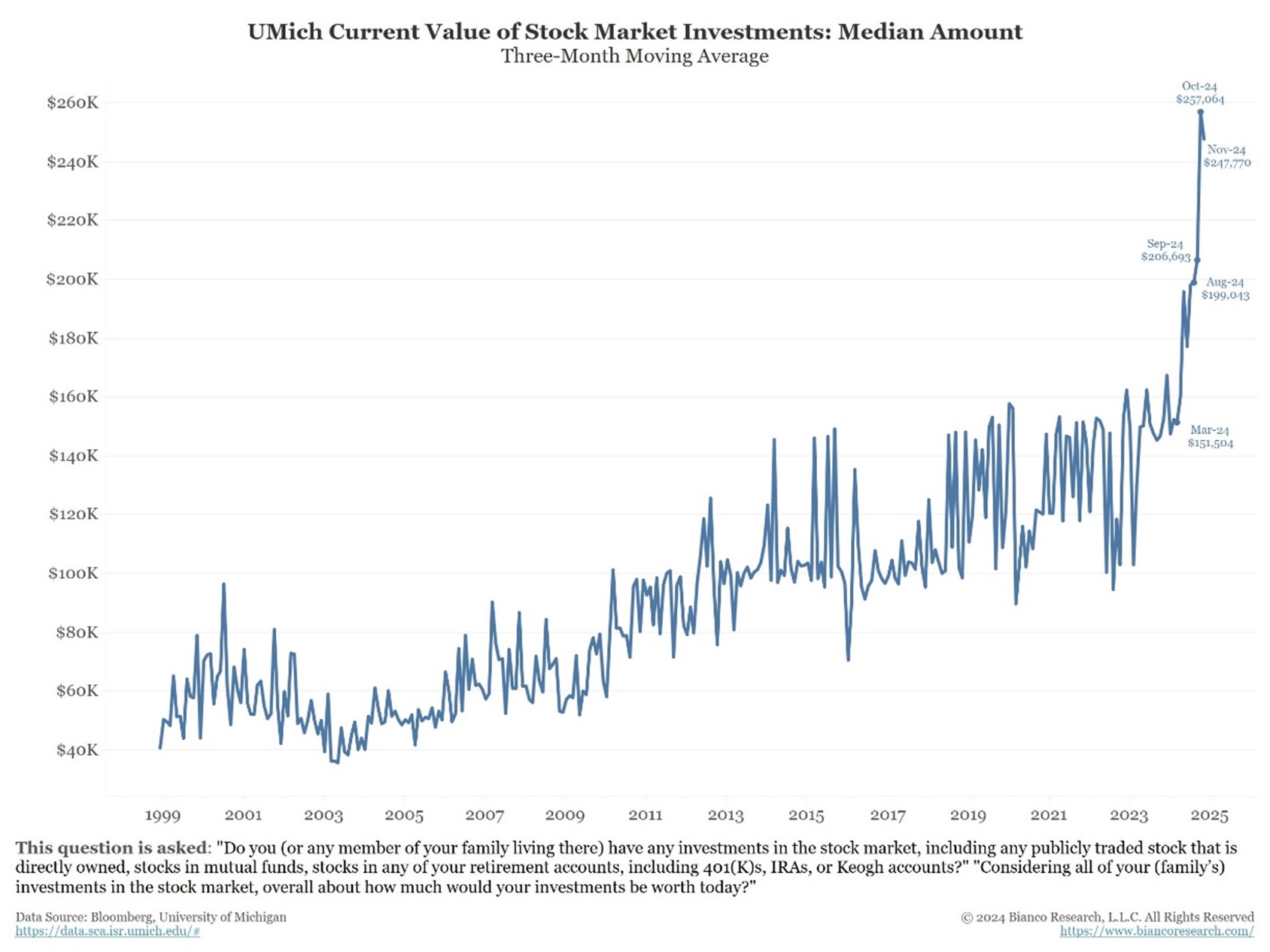

The coming year will be much different than the last two for investors. Economists predicted a 90% chance of recession in 2023. The economy really was that close. Every day that it did not was a day the undervalued stock market rose. Entering 2024, economists expected GDP growth of just 1.5%. Once again, low expectations set up more opportunities. Recession odds are near zero as we enter 2025. Americans have never had more money in the stock market. It is the opposite of the previous two years.

My system is signaling caution, prompting me to make changes. I did not wait for 2025. If stock prices continue higher, I will gratefully accept the gains by making additional adjustments. If they fall, I plan to reinvest back to normal levels.

The S&P 500 is up 0.3% in the first half of December. The largest companies get the largest weighting in this index. The equally weighted version has declined by 2.5%. This discrepancy is significant and has spotted opportunities in my system. I’ll discuss this in the “Emerging Opportunities” section.

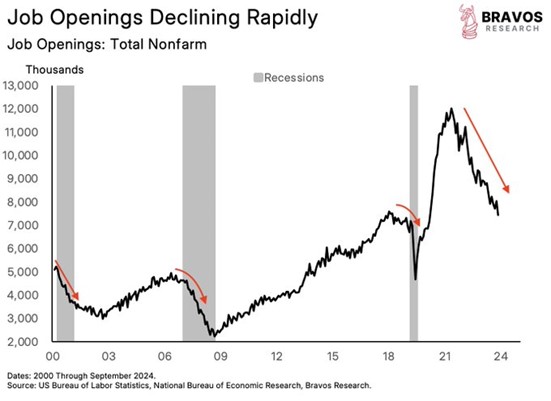

The labor market could significantly impact the economy and asset values, including housing. Government data suggests stable employment, but cracks are appearing. Full-time jobs are being replaced by part-time positions, and job openings on Indeed have dropped 38% year-over-year, the lowest since August 2020, down 49% from their February 2022 peak.

Employment becomes a concern when the 4-week average of initial jobless claims exceeds 250,000. Currently, weekly claims are at 242,000, below this threshold. The 4-week average also remains below 250,000.

The University of Michigan reports that Americans are heavily invested in stocks, a rare level of excitement. Global investors are driving stock prices up. Every buy is also a sell, with prices moving based on the more enthusiastic party. Corporate insiders and asset managers are selling, as the Commitment of Traders report indicates. This momentum may shift.

Alan Greenspan’s “irrational exuberance” from the late 1990s could persist or rise. Avoid FOMO by not buying into the most crowded and overpriced sectors. Instead, focus on emerging opportunities.

Warren Buffett advises being fearful when others are greedy and vice versa. His company, Berkshire Hathaway, has been gradually selling stocks and adding to short-term bonds all year. He seems content on missing out.

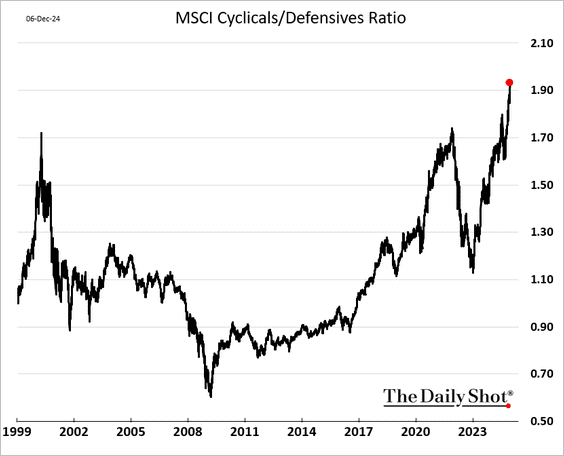

There’s a significant divergence between cyclical and defensive stocks, similar to but more compelling to me than large vs. small or U.S. vs. international. My system identified consumer products as a “buy” on October 8, 2024. I’m holding these positions. Healthcare stocks, impacted by fears surrounding the incoming Trump administration and the NYC murder of a United Healthcare CEO, look attractive. Energy stocks, though not defensive, are becoming more appealing daily.

Healthcare, consumer products, and energy stocks are under-owned and under-appreciated. They offer the best opportunities heading into 2025. I’ve allocated tactical assets in their direction and left room for further investment under the right circumstances. I am prepared to double my allocation to any of them if my system identifies the right environment and gives me the signal. Energy is a possible candidate. I am watching it closely.