Do you remember what America was like in 2006? If we could give the year a financial theme, I would label it, “Borrow and Spend!” Buying a home was easy; no verification of employment and no down payment were necessary. An interest-only loan could be obtained without any reasonable expectation of one’s ability to repay the loan.

As a matter of fact, you could borrow up to one-hundred percent of a home’s value, skip a month’s payment, and even cash out any value that had come from the rising price of the home. Leverage was the hot financial fad! Many Americans borrowed as much as they could and bought whatever they wanted!

What a difference ten years can make. Contrast 2006 with 2016; today people are taking control of their financial situations, putting themselves in the driver’s seat, and keeping their own hands on the steering wheel. Financial responsibility is much more prevalent.

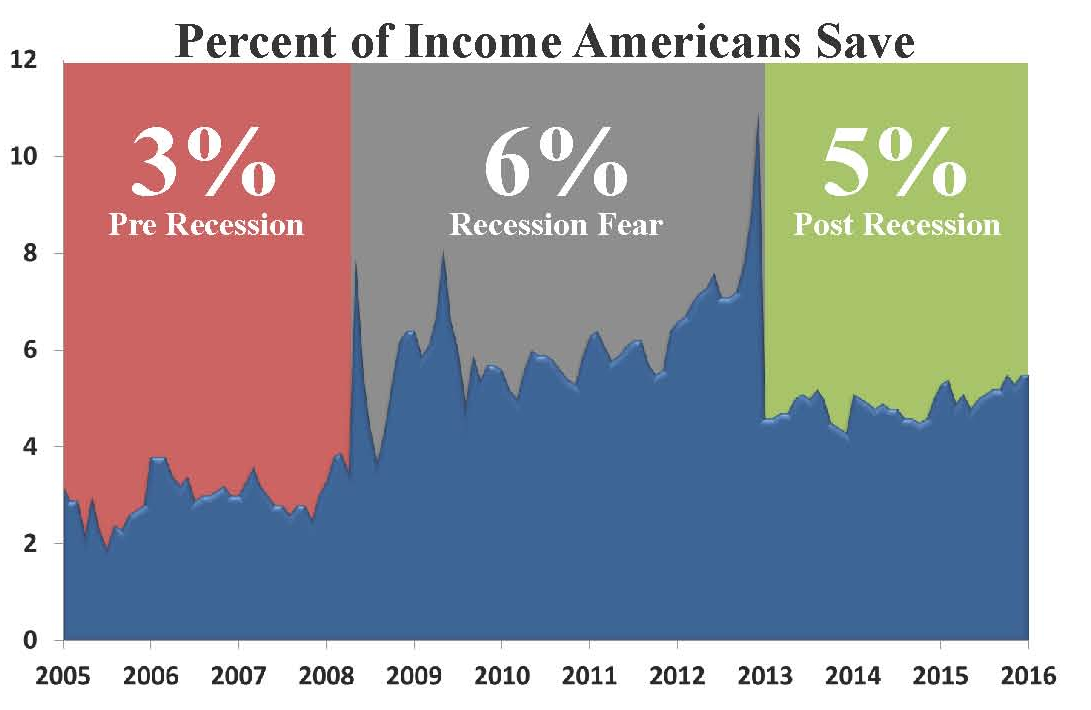

Disposable income —the money we have left to spend after taxes have been paid—has increased at an average rate of just less than one percent per year over the past ten years. So income is up a little. This makes the fact that personal saving is up very impressive. We have seen the personal savings rate increase from 3 percent at the end of 2005 to 5.5 percent at the end of 2015.

This significant improvement demonstrates a shift for Americans towards greater financial strength. Here are some of the positive outcomes.

Reduction in personal debt

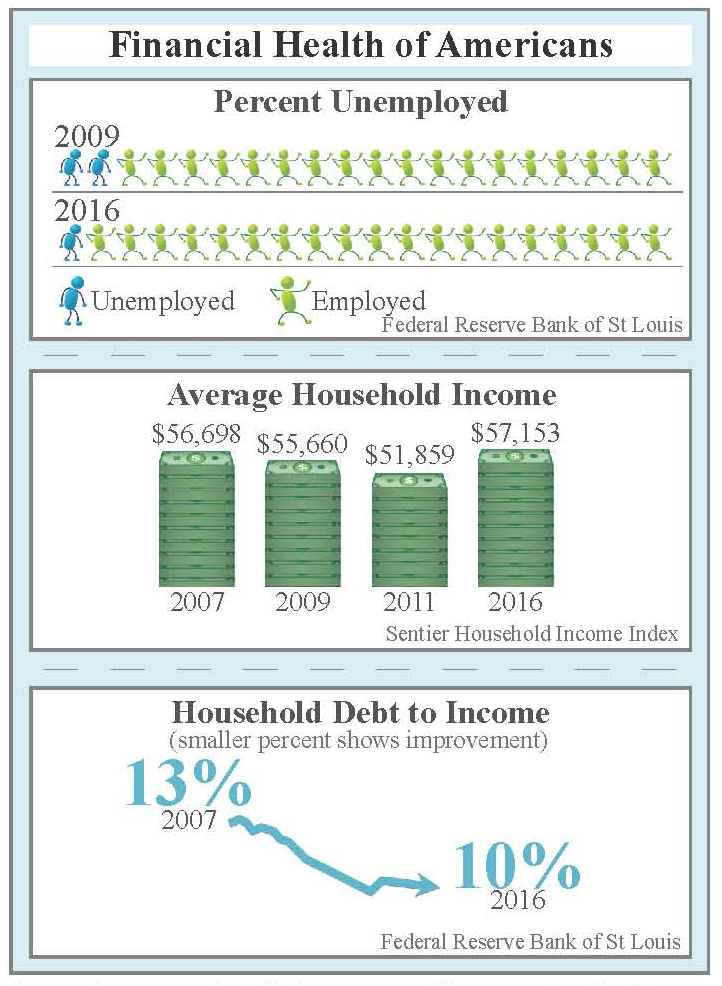

Still smarting from the financial pinch of the last recession, cash flow is now king. For many of us the perception of acceptable levels of debt has changed significantly. Debt is financial fragility, which is why Americans again recognize the value of getting out of debt as quickly as possible. Many have taken advantage of low-interest rates and refinanced to shorter-term loans. Paying off short-term loans such as car loans and signature loans is now a priority, and the use of credit card debt has reduced significantly.

Spending less

Knowing what we should do and putting it into practice can be challenging. This is especially true when it comes to living within your means. However, it is possible and it is powerful. No other financial habit is more important!

We have had the opportunity to meet with many people that have adopted the philosophy of a simpler lifestyle. This allows them to enjoy what they have without the pressure to get more “stuff” and then live with the financial burden. Managing spending also impacts our future lifestyle. If we spend everything today…what will we live on in retirement?

Increased accessible savings

After experiencing financial instability, many people have gained a witness of the need for liquidity. Access to emergency money to cover needs for 3 to 6 months has been widely recommended for decades, but it has gained new favor in the last 10 years. The wisdom of this applies beyond those still working. Retirees are also paying attention to liquid savings to make sure they can cover the unexpected emergencies that will surely come.

Focus on planning for the future

A shift has taken place in young people as well. They are saving for their futures at the beginning of their careers. Company-sponsored retirement plans such as 401(k) or 403(b), as well as individual IRA or Roth IRA, are now common to this young generation and they are off to a strong start.

Those who see retirement on the horizon have a new goal. They want to maintain a comfortable lifestyle throughout their retirement years. With fewer pension plans providing retirement income, the burden to provide income during retirement has been shifted to them. Many have hit the ceiling on contributing to their retirement plans and are using additional savings to help them reach their goals.

It is clear that over time all things can change; the market, our spending and savings habits, even our perception of what’s important financially. We have learned many valuable lessons and have made significant strides to improve our financial situations. The next ten years will undoubtedly bring more changes; some will be good and some will be bad. Remember to prepare when times are good and don’t fall prey to the next financial fad. Keep in mind that you are in the driver’s seat.